Company Overview

ImmunityBio, Inc. (NASDAQ: IBRX) is a commercial-stage immunotherapy company headquartered in San Diego and Culver City, California. Founded and led by billionaire physician-scientist Dr. Patrick Soon-Shiong, the company has pioneered the development of IL-15 receptor superagonist technology, culminating in its lead commercial product, ANKTIVA® (nogapendekin alfa inbakicept-pmln).

After nearly a decade and over $3.7 billion in cumulative losses as a development-stage entity, the company reached a commercial inflection point in April 2024 when the FDA approved ANKTIVA for BCG-unresponsive non-muscle invasive bladder cancer (NMIBC). This marked the first commercialization of an IL-15 receptor superagonist anywhere in the world.

Mission

To “activate the immune system to treat cancer like a common cold” positioning ANKTIVA as the missing link in modern oncology, complementing but not replacing checkpoint inhibitors.

Platform Technology

- IL-15 Superagonist (ANKTIVA): Cytokine fusion protein that activates T-cells and NK cells, driving immunological memory against tumors

- t-haNK CAR-NK Cells: Off-the-shelf allogeneic NK cell therapy platform (no lymphodepletion required)

- DNA/mRNA Vaccine Vectors: Used in infectious disease and cancer vaccine programs

- Recombinant BCG (rBCG): Partnership with Serum Institute of India to address global BCG shortage

Lead Product ANKTIVA® (nogapendekin alfa inbakicept)

FDA-Approved Indication

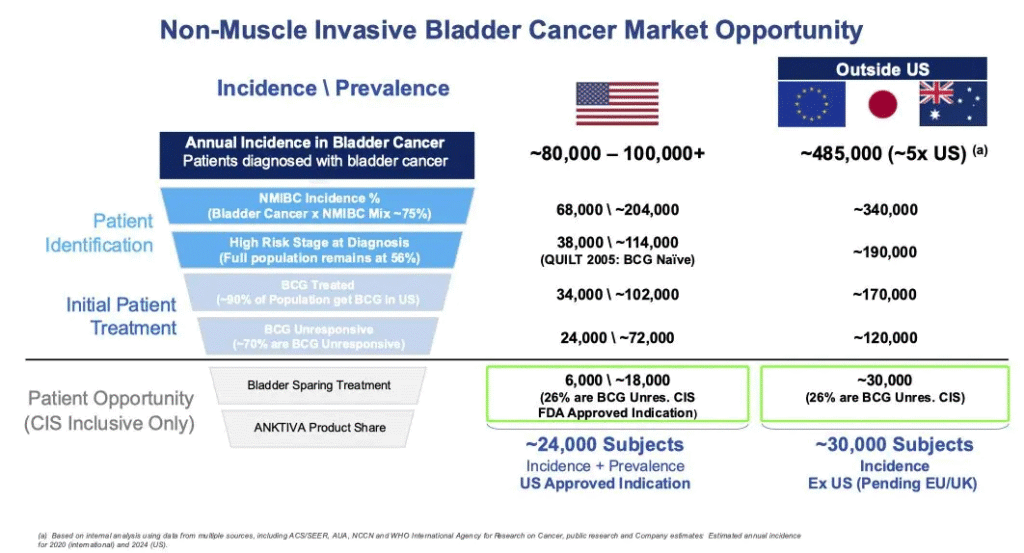

ANKTIVA + BCG for adult patients with BCG-unresponsive NMIBC with carcinoma in situ (CIS), with or without papillary tumors. FDA approval granted April 2024; J-code assigned mid-2024, accelerating commercial uptake.

Commercial Momentum

- FY2025 product revenue: ~$113M, a ~700% year-over-year increase

- Q4 2025 revenue: $38.3M (vs. $7.6M in Q4 2024)

- Unit sales grew approximately 750% in 2025 vs. 2024

- Gross margins on ANKTIVA are exceptionally high (~99%) due to biologics manufacturing economics

- Rapid penetration of U.S. urology market as the only approved option for BCG-unresponsive NMIBC CIS

Global Regulatory Approvals (33 Countries)

- United States: FDA approved April 2024 (NMIBC CIS)

- United Kingdom: MHRA authorization

- European Union: European Commission conditional marketing authorization (Dec 2025) EU Pharma Package incentives if launched in all 27 member states within 2 years

- Saudi Arabia (SFDA): NMIBC CIS and metastatic NSCLC approvals, world’s first NSCLC approval for ANKTIVA + checkpoint inhibitor

Financial Analysis

Revenue Trajectory

The revenue ramp is among the most impressive in recent small-cap biotech history:

| Quarter | Revenue | QoQ Change | EPS Loss |

| Q4 2024 | $7.6M | — | -$0.08 |

| Q1 2025 | $16.5M | +117% | -$0.15 |

| Q2 2025 | $26.4M | +60% | -$0.10 |

| Q3 2025 | $32.1M | +22% | -$0.07 |

| Q4 2025 | $38.3M | +19% | -$0.06 |

| FY2025 Total | $113M | +700% YoY | -$0.38 (TTM) |

Balance Sheet & Cash Position

- Cash and marketable securities: ~$242.8M as of December 31, 2025

- Net loss FY2025: -$351.4M (down 15% vs. 2024 loss, reflecting operating leverage improvements)

- Quarterly net loss improving each quarter: from -$92M in Q1 down toward ~$62M in Q4

- Negative shareholders’ equity (accumulated deficit >$3.7B)

- At current quarterly burn of ~$80-92M, the cash runway is estimated at less than one year without additional financing

Funding Structure & Dilution Risk

This is one of the most significant risks for existing shareholders. ImmunityBio’s capital structure is complex and founder-dependent:

- Dr. Patrick Soon-Shiong holds approximately 66% of outstanding shares — extreme insider concentration

- $505M convertible note due December 2027 held by Soon-Shiong’s private entities

- $164.2M in potential CVR cash obligations outstanding

- Royalty-backed financing with Oberland Capital adds further obligations

- Historical dilution: approximately 37% over the prior 18 months (as of Oct 2025); continued ATM equity offerings expected

- Every financing round or convert triggers further share count expansion, eroding per-share value

Competitive Landscape

NMIBC Current & Near-Term Threats

| Competitor | Product | Mechanism | Status | Threat Level |

| Johnson & Johnson | Inlexzo (TAR-200) | Targeted drug delivery (intravesical) | FDA approved, commercially scaling | HIGH: superior efficacy data in some comparisons; J&J commercial muscle |

| Merck | Keytruda (pembrolizumab) | PD-1 checkpoint inhibitor | Approved for various bladder cancers; label expansion studies ongoing | MEDIUM: not same indication but physician familiarity strong |

| BMS | Opdivo (nivolumab) | PD-1 checkpoint inhibitor | Bladder cancer approvals | MEDIUM: indirect competition |

| UroGen | Mitomycin / UGN-102 | Intravesical chemo | Approved for LG-NMIBC | LOW-MEDIUM: different segment |

ANKTIVA’s Competitive Advantages

- Only FDA-approved therapy for BCG-unresponsive NMIBC CIS, first-mover advantage with established prescriber relationships

- Superior duration of complete response vs. historical controls, 9-month CR of 84% vs. 52% for BCG alone in BCG-naïve trial

- No chemotherapy, manageable safety profile, attractive for elderly bladder cancer population

- Recombinant BCG development addresses global BCG shortage, which is a key supply dependency risk turned strategic asset

- IL-15 mechanism is differentiated from and complementary to checkpoint inhibitors, combination potential

- RMAT Designation from FDA for ANKTIVA in lymphopenia reflects strategic government interest

Key Competitive Risk: J&J’s Inlexzo

Johnson & Johnson’s Inlexzo (TAR-200) represents the most direct near-term competitive threat. Bears argue it demonstrates superior efficacy data and benefits from J&J’s massive oncology sales infrastructure and physician relationships. If Inlexzo captures a significant share of the BCG-unresponsive NMIBC CIS market, it could cap ANKTIVA’s U.S. revenue growth ceiling significantly below bull-case estimates.

Key Upcoming Catalysts (2026)

| Timeline | Catalyst | Impact | Direction |

| Mar 3, 2026 | FY2025 Full Earnings Report & Business Update Call | HIGH | Binary |

| Q1 2026 | sNDA submission for papillary NMIBC label expansion (no new trial needed) | HIGH | Positive |

| Q1/Q2 2026 | Recombinant BCG (rBCG) regulatory submission, Saudi Arabia & FDA | MEDIUM | Positive |

| H1 2026 | Full enrollment completion: QUILT-2.005 (BCG-naïve NMIBC CIS) | HIGH | Positive |

| 2026 | NSCLC Phase 3 design announcement / IND filing | HIGH | Binary |

| Q4 2026 | BLA submission target: BCG-naïve NMIBC (1L label) | VERY HIGH | Very Positive |

| Dec 2027 | $505M convertible note maturity, refinancing/repayment required | VERY HIGH | Binary (dilution risk) |

| Ongoing | GBM Phase 2 data updates; CAR-NK enrollment progress; EU commercial launch data | MEDIUM | Positive |

Management & Governance

Dr. Patrick Soon-Shiong, Founder, Executive Chairman & CEO

Billionaire physician, scientist, and entrepreneur. Previously sold APP Pharmaceuticals and Abraxis BioScience to Fresenius and Celgene respectively, generating billions in personal wealth. Controls approximately 66% of IBRX shares. Has a history of self-funding biotechs and tolerating extreme dilution to achieve scientific goals.

Key governance concern: Soon-Shiong’s private entities have provided financing through promissory notes and have received royalty-backed deals from ImmunityBio. While he has demonstrated commitment to the company, this structure creates potential conflicts between minority shareholders and the controlling shareholder.

Insider Activity (Recent)

- Director Christobel Selecky sold 25,000 shares on Feb 23, 2026 at ~$10

- Director Barry J. Simon sold 175,000 shares on Feb 20-23, 2026 for ~$1.78M

- Multiple Form 4 filings in February 2026 suggest insider selling into the rally

Insider selling at these levels is notable as a caution signal, though directors selling modest amounts near 52-week highs is common practice and not necessarily indicative of fundamental deterioration.

No responses yet